Capital gain on sale of immovable property

- Introduction: It is important to determine that when it can be termed as capital gain on sale of immovable property and whether it will be classified as long term or short-term; further what will be the rate at which it will be taxable.

- Capital asset is defined to include:

(a) Any kind of property held by an assessee, whether or not connected with business or profession of the assessee.

(b) Any securities held by a FII which has invested in such securities in accordance with the regulations made under the SEBI Act, 1992.

However, the following items are excluded from the definition of “capital asset”:

(i) any stock-in-trade (other than securities referred to in (b) above), consumable stores or raw materials held for the purposes of his business or profession;

(ii) personal effects, that is, movable property (including wearing apparel and furniture) held for personal use by the taxpayer or any member of his family dependent on him, but excludes (i.e. this item will be treated as capital asset) jewellery; archaeological collections;drawings;paintings;sculptures; or any work of art.

“Jewellery” includes ornaments made of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals, whether or not containing any precious or semi-precious stones, and whether or not worked or sewn into any wearing apparel;precious or semi-precious stones, whether or not set in any furniture, utensil or other article or worked or sewn into any wearing apparel;

iii) Agricultural Land in India will not be treated as capital asset, however, if it is;

- Within jurisdiction of municipality, notified area committee, town area committee, cantonment board and which has a population of 10,000 or more;

- Within range of following distance measured aerially from the local limits of any municipality or cantonment board:

- up to 2 KMs, if population of such area is more than 10,000 but not exceeding 1 lakh;

- up to 6 KMs in case where population of such area is more than 1 lakh but not exceeding 10 lakhs; or

- not being more than 8 KMs, if population of such area is more than 10 lakhs. Population is to be considered according to the figures of last preceding census of which relevant figures have been published before the first day of the year

2.1 Classification:

Generally, Short-term Capital Asset means capital asset held by the assessee for less than 36 months immediately before the date of transfer, Thus Long-term Capital Asset means a capital asset held for more than 36 months. However, in case of Capital Asset being Land or Building this period will be taken as 24 months instead of 36 months.

Profits arising on a transfer of short-term capital asset are liable to tax as any other incomeon the other hand; gains arising on transfer of long-term capital asset are taxed at the rate of 20%after allowing the benefit of indexation. Thus, classification of an asset as a long-term or short-term asset is therefore of considerable importance.

- For the purpose of computing capital gains , the capital asset is bifurcated into two categories on the basis of the duration for which they have been held by the assessee, namely:

- Short-term Capital Asset.

- Long-term Capital Asset.

2.2 Cost of Acquisition:

Cost of acquisition will be consideration paid by the seller however there may situation where seller has not incurred the cost (e.g. property inherited to the owner) in such cases cost will be the cost to previous owner; such cases can be as follows:

Where the capital asset became the property of the assessee-

- on any distribution of assets on the total or partial partition of a Hindu undivided family;

- under a gift or will;

- by succession, inheritance or devolution, or on any distribution of assets on the liquidation of a company, or under a transfer to a revocable or an irrevocable trust.

- Transaction in shares in relation to amalgamation of Indian company or transaction relating conversion of debenture into share.

2.4 Exemptions:

| Relevant Section | Condition | Exemption available |

| Section 54 |

|

Maximum Exemption will be up to the amount of capital gain. |

| Section 54F |

|

Proportionate exemption will be available if total net sale proceeds are invested then in that case full capital gain will be exempted. |

| Section 54EE |

|

Maximum Exemption will be up to the amount of capital gain. Further it will be still subject to monetary limit of RS 50,00,000/-. |

| Section 54EC |

|

Maximum Exemption will be up to the amount of capital gain. Further it will be still subject to monetary limit of RS 50,00,000/-. |

| Section 54B |

|

Maximum Exemption will be up to the amount of capital gain. |

- 194-IA: “TDS on Immovable property”

- Whether person is required to deduct TDS in case of sale of immovable property?

According to section 194-IA any person, being a transferee (Buyer), responsible for paying to a resident transferor (Seller) any sum by way of consideration for transfer of any immovable property (other than agricultural land i.e. not required to deduct TDS in that case) shall deduct an amount equal to 1%.

- When such person is required to deduct TDS?

The transferee will be required to deduct a sum as income-tax at the time of credit of such sum to the account of the transferor or at the time of payment of such sum in cash or by issue of cheque or draft or by any other mode, whichever is earlier.

- Whether there is any monetary limit or threshold limit?

Deduction will be required only in case where consideration for the transfer of an immovable property is less than 50,00,000/-.Further this limit is not exemption limit i.e. he will be required to deduct TDS on entire amount in case were consideration exceeds Rs. 50,00,000/

- Which form is required to be furnished in case of TDS deduction under above section? Within how many days such tax is required to be deposited?

The Tax so deducted is to be has to be deposited within 7 days from the end of the month in which the tax was deducted. Tax is to be accompanied by a challan-cum-statement in Form 26QB, electronically, within the specified time. Further, every person responsible for deduction of tax u/s 194IA shall furnish a certificate of TDS in Form 16B to the payee within 15-days from the due date for furnishing the challan-cum-statement in form 26QB.

- Question that may arise

- Mr Doshi has sold his residential flat; apart from this flat he was not holding any house; he has earned income of Rs. 60,00,000 due to sale this flat in form of capital gain? What are the deduction that can be claimed by Mr. Doshi and that will create optimum benefit for them?

In this case Mr. Joshi can buy another house property and can claim benefit under section 54 (as prescribed above. Further Mr. Doshi can invest in specified bond and unit but in that case maximum monetary limit for him will be Rs. 50,00,000/- and there is no restriction that he cannot claim both the benefit; therefore, Mr. Doshi can also claim benefit of both sections simultaneously

- What if in the above case Mr. Doshi has sold his plant and machinery and he wants to avail deduction by investing in house property. Whether he can do so? What are the other remedy that is available with Mr. Doshi?

In that case Mr. Doshi is eligible to claim exemption but to claim full exemption i.e. of Rs. 60,00,000/- he is required to invested entire net sale proceed in to new residential house property as exemption will be available under section 54F which provides proportionate deduction. Further Mr. Doshi can invest in specified bond and unit but in that case maximum monetary limit for him will be Rs. 50,00,000/- and there is no restriction that he cannot claim both the benefit; therefore, Mr. Doshi can also claim benefit of both sections simultaneously.

- What if in above case Mr. Doshi is holding more than one house property and he has capital gain on sale of plant and machinery?

In that case Mr. Doshi will not be eligible to claim exemption as specified under section 54F but still Mr. Doshi will be eligible for exemption as specified under section 54EE/54EC.

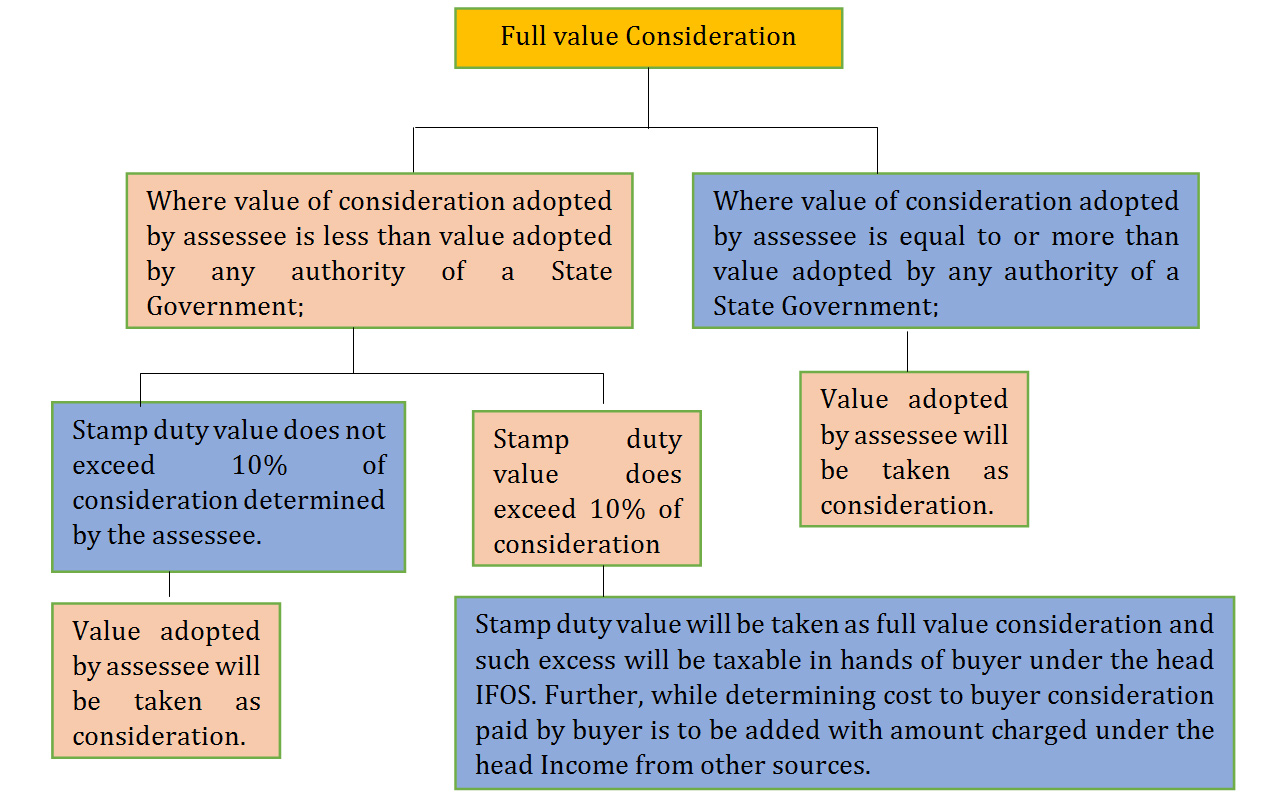

- Raj has sold a Land the consideration received by him is Rs. 30,00,000/- Mr Devi is purchaser of property has communicated with Mr. Raj that he will deduct TDS on the above payment as Stamp Duty Value (SDV) adopted by the government authority is Rs. 51,00,000/-. Determine the consequence on tax liability.

In the given case Mr. Raj has to compute capital gain by considering full value consideration as Rs. 51,00,000/- i.e. stamp duty value will be taken as full value consideration as the difference between original consideration and stamp duty is value is more than 10%; Further such excess i.e. Rs. 21,00,000 will be taxable in hands of Mr. Devi under the head ‘Income from other sources’ Also, while determining cost to buyer consideration paid by buyer is to be added with amount charged under the head Income from other sources.

The deduction of TDS is governed by section 194IA and it specifically determines consideration paid by the buyer. Therefore, in the given case Mr. Devi is not required to deduct TDS.

- What if in the given case Stamp Duty Value (SDV) adopted by authority is Rs. 32,00,000/-

In that case Mr. Raj has to compute capital gain by considering full value consideration as Rs. 30,00,000/- i.e. in that case section 50C (considering stamp duty value in case full value consideration and stamp duty value has difference of more than 10%) will not be applicable. Further nothing will be taxable in hands of Mr. Devi and cost of acquisition for him will be Rs. 30,00,000/-. In this case as consideration does not exceeds the limit specified under section 194IA, Therefore, no TDS is required to be deducted.

- Raj is inherited with as house; this house was purchase by his farther in 1989 the cost incurred by them to purchase house was Rs. 25,000/- after that he incurred repairing cost of Rs.20,000/- in year 1999 after that he further incurred repairing cost of Rs.50,000/- in year 2009-10. Fair value as on 01-04-2000 was Rs. 80,000/- what will be cost of acquisition for Mr. Raj in case he has sold his house under financial year 2019-20.

In the given case assessee is provided with option that he can take either FMV as on 01-04-2000 or he can take actual total cost incurred including repairing cost incurred by the assessee. Assuming Mr. Raj will select the higher of two i.e. Rs. 80,000/- that will be multiplied with indexation of year 2019-20; and will be divided by indexation of year of purchase and in case where FMV as on 01-04-2000 is adopted by 100. Therefore, in given case it will come Rs. 2,31,000/- (80,000*(289/100) and further any repairing expense incurred after 01-04-2000 will be considered and therefore, indexed cost of repairing will be Rs. 97,635/- (50000*289/148).