Assessment under Goods and Service Tax (GST)

Introduction: It is important to know that how person is assessed under various provision of GST, whether assessee has an option to opt for provisional assessment or not; in which cases GST authority will considered the case under best judgement assessment; or what are the provision relating to assessment of unregistered person. In this article we will discuss all such provisions along with relevant illustration.

Definition:

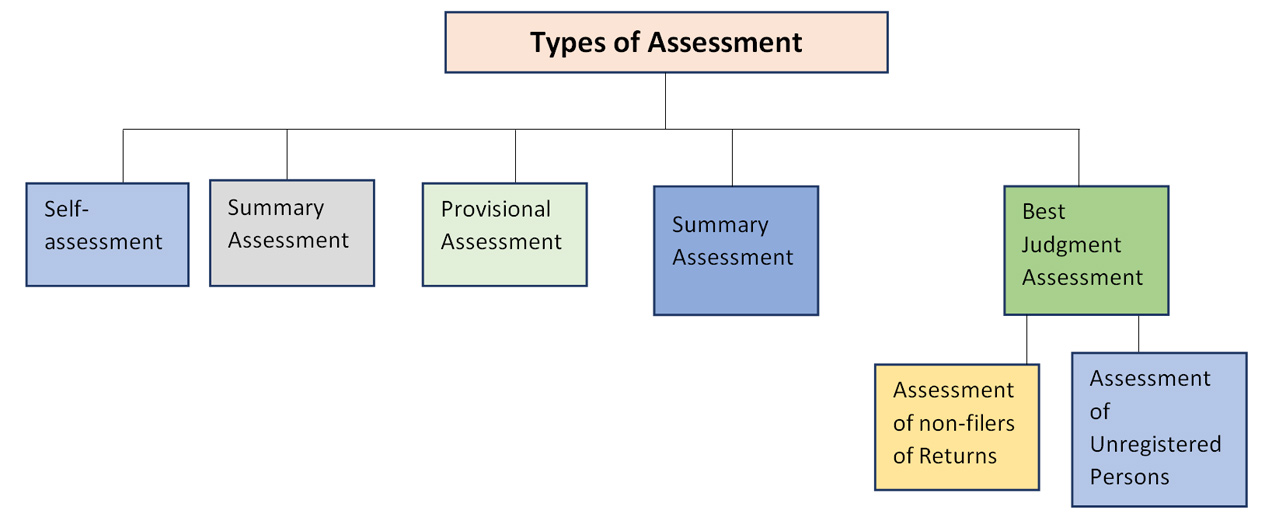

Assessment: It meansdetermination of tax liability under this Act and includes self-assessment, re-assessment, provisional assessment, summary assessment and best judgment assessment.

It is mandatory for the person to determine the tax liability based on self-assessment, and to pay the tax while filing return under GST.

Self-assessment (Section 59) : Every person who is a registered has to assess his tax liability on his or her own calculations and application of provision of law and shall furnish returns for each taxation period. The amount which assessee arrives after self-assessment shall be paid by him by way of furnishing return of income.

Provisional-assessment (Section 60): If an assessee is unable to determine his tax liability, or value of supply or rate of tax then he can request the officer for provisional assessment. Therefore, in cases where person is not able to determine transaction value or unable to determine the rate of tax due to difficulty in classification of goods and services or due to not able to determine applicability of notification, he may apply for provisional assessment.

Illustration : Mr. J has supplied service to Mr. T who is unregistered person, Mr. J is not sure about rate that will be applicable to him, he has also consulted with one of friend but he is still not sure. Whether he can apply for provisional assessment?

If in any case assessee is not able to determine transaction value or unable to determine the rate of tax due to difficulty in classification of goods and services or due to not able to determine applicability of notification, he may apply for provisional assessment. In the given case Mr. J can apply for provisional assessment.

What if in the given case instead of rate Mr. J is unable to determine place of supply. Whether still he can apply for provisional assessment?

In that case Mr. J will not be able to apply for provisional assessment. It is advisable to Mr. J that he shall pay the tax on Self-assessment basis and then by virtue of section 77 of CGST Act, 2017; where he is allowed to adjust the supply considered as intra-state as inter-state and inter-state as intra state and no interest is also levied for the same.

What is the procedure for applying under provisional assessment?

- The assessee has to request the GST officer for provisional assessments in writing.

- Within 90 days of receipt of such request the officer will pass an order after reviewing the application. This order is for allowing a payment of tax on provisional basis or at a GST rate or value specified by him.

- The assessee who is making payment on provisional basis has to issue a bond with a security promising to pay the difference amount between provisionally assessed tax and final assessed tax.

- The GST officer will pass the final assessment within a period of six months from the date of order of provisional payment. The commissioner can even extend this time period to 4 years if required.

- After the final assessment assessee is required to pay the difference amount if any with interest at the rate of 18% per annum and if he has paid more then the amount required under final assessment then he will be refunded back with the same amount as well as interest will be paid on such refund at the rate 6% per annum.

Summary Assessment (Section 64): The authorized officer is after obtaining prior permission of additional commissioner or joint commissioneron any evidence showing a tax liability of a person coming to his notice, proceed to assess the tax liability of such person to protect the interest of revenue and issue an assessment order, if he has sufficient grounds to believe that any delay in doing so may adversely affect the interest of revenue. The order of summary assessment is issued under GST ASMT-16 and assessee has an option to file an application in form ASMT-17 within 30 days from receipt of order of commissioner. The Commissioner has power to withdraw such order if he consider it as erroneous.

Best Judgement assessment:

- Assessment of non-filers of returns (Section 62) : When a registered person fails to furnish the required returns, even after service of notice an assessment would be conducted by the GST Officer. In such cases, the GST officer would proceed to assess the tax liability of the taxpayer to the best of his judgement taking into account all the relevant material which is available or which he has gathered and issued an assessment order within a period of five years from the date for furnishing of the annual return for the financial year to which the tax not paid relates.

On receipt of the said assessment order, if the registered person furnishes a valid return within a period of 30 days from the date of issuance of assessment order, then in such case, the assessment order would deemed to have with drawn. However, the registered person will be liable to pay interest and late fee if any.

Illustration : Mr. Jive has is registered under GST as Normal Taxpayer he has not furnished GSTR Returns for 8 previous months. GST officer has taken the case under section 62 and has passed the assessment order determining the liability of the taxpayer to the best of his judgement taking into account all the relevant material which is available or which he has gathered and issued an assessment order. On receipt of said order Mr. Jiva furnished all the pending returns withing 30 days from date of issuance of assessment order. GST officer denied such filling and ask to pay tax as determined under assessment order. Whether the contention of GST officer is valid.

In the given case contention of GST officer is not valid as it has been stated under section 62 of CGST Act, 2017 that if the assessee is filling all the pending return within 30 days from the date of issuance of assessment order, then the assessment order under section 62 would be deemed to be invalid. Therefore, contention of GST officer is invalid.

- Assessment of unregistered Persons (Section 63) : When a taxable person fails to obtain registration even though he is liable to do so or where registration of person

}n has been cancelled even if he is liable to pay tax GST officer can process his or her tax liability to the best of his judgement. The officer can issue an assessment order within five years from the due date for furnishing annual return for the financial year for which taxes are unpaid.

Illustration : Mr. D has turnover of Rs. 60,00,000/- during the financial year 2018-19, he has not obtained registration under GST as he is suffering from loss in business, he is of the view that GST registration is not required. Whether the contention of Mr. D is valid? Whether GST officer has power to determine the liability of such unregistered person? If yes what will be the time limit within which order is required to be issued.

In the given case contention of Mr. D is not valid in eye of law as GST registration is mandatory if the turnover of assessee exceed the limit specified under section 22 of CGST Act, 2017; The GST officer can consider the above case under section 63 of CGST Act, 2017; i.e.assessment of unregistered persons and can determine his or her tax liability to the best of his judgement.officer can issue an assessment order within five years from the due date for furnishing annual return for the financial year for which taxes are unpaid.

Summary assessment (Section 61):Whenever any return is furnished it is necessary for the department to verify the correctness of the returns and therefore GST officer will scrutinize it. Such scrutiny is covered under section 61 of CGST Act, 2017. After scrutiny if any discrepancy found, GST officer will furnish the notice to the registered persons about the discrepancy and seeking the reply from the person. And the said person shall within 15 days from the date of the notice furnish explanation in form of reply or he may accept the discrepancy as mentioned in the notice and pay the taxes, interest and any other amount due and inform the same to proper officer.

In case if assessee instead of accepting discrepancy furnishes the reply then proper officer has to determine that information is acceptable or not. If proper officer finds that information provided by the person is satisfactory then he may drop the proceedings and if he is not satisfied, he may initiate recovery by either conducting special audit of assessee or by issuing notice as per section 73 i.e. cases other than willful defaulter or under section 74 i.e. cases of will ful defaulter