Introduction : Whenever any movable or immovable property is given in form of gift the first question arises in mind of receiver is taxability of such gift under Income Tax Act, 1961; There are certain exemption which are provided to assessee in respect of gift received by him and there is also specific monetary limit stated by government for any financial year. Therefore, lets analysis provision specified by the government in this regard:

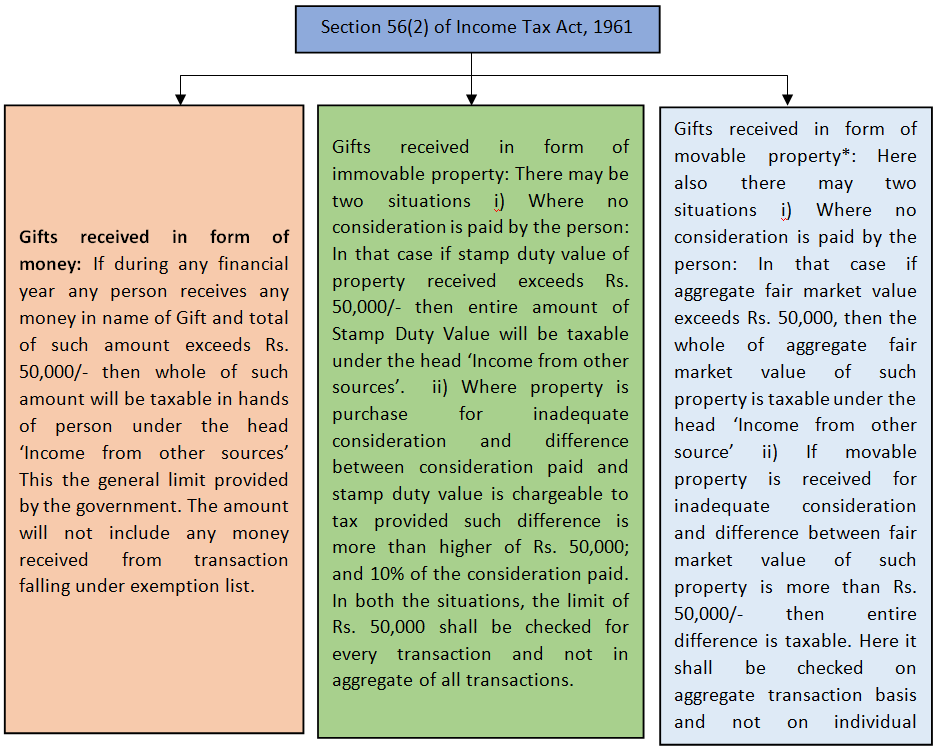

Provision relating to taxability of Gifts:

*Movable Property has been defined as any property in the nature of Shares and securities, Jewellery, archaeological collections, drawings, paintings, sculptures, any work of art, or bullion. Therefore, if there is any other movable property such as Car, Watch, etc. then it will not be taxable.

Exemptions which are available to assessee

- If gift has been received on the occasion of the marriage of the individual or under a will or by way of inheritance.

- If gift has been received from any specified relative or from any local authority. Relative for the purpose means

Wife of the individual; Brother or Sister of the Individual; Brother or Sister of the Wife of the Individual; Brother or Sister of either of the parents of the Individual; Any lineal ascendant or descendant of the Individual; Any lineal ascendant or descendant of the wife of the Individual; wife of the person referred to in any of the above persons.

- Gift received from any trust or institution registered under section 12A/12AA/12AB or by any trust or institution registered under section 12A/12AA/12AB.

- Also, there are many other exemptions which are applicable in case of amalgamation/merger or demerger.

Important Points:

- Whenever employer is providing any gifts to his employee such gifts are not taxable if the amount of such gift does not exceeds Rs. 5,000/-. However, if value of such gift is exceeding Rs. 5,000/- then such excess amount is chargeable as salary Income.

- Also if we see from point of view of GST then as per section 7 of CGST Act, 2017; any transfer, barter, sale, lease, exchange by whatever name called will be treated as supply but such supply shall be for consideration; now, if any item, article, asset if it is supplied as gift and no consideration is received then in that case GST will not be applicable on such supply. Further, credit relating to such inputs which are used in such supply, will also be blocked by purview of section 17(5) of CGST Act, 2017. But if such supply is for inadequate consideration then in that case as per section 15 transaction value will be deemed to the consideration received/receivable by the supplier and in that case, GST will be levied on transaction value. Here it is assumed that transaction between the parties are not related parties as per definition prescribed in GST

- If in the above case parties to transaction are related party then in such case, even if considerationis not received Schedule 1 of CGST Act, 2017 specifies that any sale, transfer, barter, lease, exchange by whatever name called between related party even if it is without consideration it will be treated as supply and for determining value of consideration CGST Rules, 2017 is to be referred.

- In India provision of Gift are governed by section 56(2) of Income Tax Act, 1961; Accordingly, irrespective of class and residential status of assessee taxability of Gifts will be governed by this section. It is important to note that previously any gift by resident to non-resident (irrespective whether given in form of money or otherwise in form of any asset) was out of the purview of taxation as it was claimed by the non-resident that such gifts are not covered under Income Tax as it does not accrues or received in India; however after this section 9 of Income Tax Act, 1961 is amended andnow income shall be deemed to accrue or arise in India if it arises due to payment of money without adequate consideration, by a resident person to a non-resident (Only amount in excess of 50,000/- will be taxable). Even after providing amendment under section 9 of Income Tax Act, 1961; such amendment does not cover transfer of movable/immovable property by resident to non-resident; therefore, if any property is transferred (whether movable or immovable) by resident to non-resident such will not be covered under said section and hence, will not be liable to taxability. (as there is no clarification regarding such)

Illustrations: Mr. X has received wrist watch from his employer the value of such watch is Rs. 20,000/-. Whether such will be taxable in hands of Mr. X? If yes, under which head of income?

In the given case this gift provided by employee to employer and such gift will be taxable if the value of gift exceeds Rs. 5,000/- in case no consideration has been received. Therefore, such gift will be taxable in hands of Mr. X under the head Income from Salary amounting to Rs 15,000/-

Illustrations: Mr. R has received share from his friend the fair market value of such is Rs. 30,000/-. Whether shares will be taxable in hands of Mr. R? If yes, under which head of income?

In the given case, shares fall under the definition of movable property and therefore in case of no consideration and if amount of fair market value of such shares exceeds Rs. 50,000/- then it will be taxable under the head Income from Other Sources. The value in question is not exceeding the limit, therefore no tax liability will arise in hands of Mr. R.

Illustration: Mr. D has purchase two house property i) Stamp duty value is Rs. 40,00,000/- Consideration paid Rs. 37,00,000/- ii) Stamp duty value is Rs. 6,00,000/- Consideration paid Rs. 5,40,000/-. How the amount will be taxable in hands of Mr. D?

In the given case for the first property difference between stamp duty value and amount of stamp duty value is of Rs. 3,00,000/-. This is to be compared with 10% of Rs. 37,00,000/- or Rs. 50,000/- whichever is higher, if the difference is more than Rs 3,70,000 then entire difference is taxable. In case one there will not be any addition to income as difference is not exceeding Rs. 3,70,000/-; but in case two difference between stamp duty value and amount of stamp duty value is of Rs.60,000/- which is more than Rs. 54,000/- (i.e. higher of Rs. 54,000/- and 50,000/-) Therefore entire difference will be taxable under the head Income from other source. Further now cost of acquisition for Mr. D will be Rs. 6,00,000/-. It is important to note the limit of Rs. 50,000 and 10% of consideration paid shall be checked for every transaction and not in aggregate of all transactions.

Illustration: Mr. G has received an amount of Rs 1,00,00,000/- as Gift from his Uncle (Brother of Father) in the occasion of Marriage – is it taxable? Similar situation but gift is received in the occasion of Birthday – Is it taxable?

In the given case irrespective of amount and nature of relationship if any Gift has been received by the assessee on occasion of marriage then in such case he will be covered under the exemption and no taxability on such gift will arise. However, if such gifts are received in occasion of birthday it will be taxable.

Illustration: Mr. Desai has created a private discretionary trust for his child and the said trust has received an amount of Rs 50,00,000/- in form of gift from the beneficiary’s Aunty (Sister of Mother of Beneficiary) – Is it taxable?

In the given case only trust which are registered under section 12AA/12AB is covered under the exemption i.e. any gift received by said registered trust will be exempted; however, the said exemption does not cover private discretionary trust. Due to this, the said transaction will fall under general provisions and in that case any gift received in cash and the amount exceeds Rs. 50,000/- then the said will be taxable because trust is separate legal entity and it’s provision of gift received from relative is applicable only to individual and HUF. In such case Rs. 50,00,000/- will be treated as taxable income in hands of trust.

Instead of such transfer from the beneficiary’s Aunty it is advisable that she shall transfer amount directly to child’s account as this will fall under the definition of relative and the said transaction will be treated as exempt transaction.

Illustration: Mr. X has received Rs 50,00,000/-as gift in cash, in XYZ HUFfrom Trust registered under Section 12A/12AA/12AB. Whether such will be taxable in hands of XYZ HUF? Whether the said transaction will be treated as taxable if Mr. Xis a trustee in such trust – Is it Taxable?

If gift is received by HUF from any of the trust registered under section 12AA/12AB then in that case said transaction will be covered under exemption and such will not be taxable in hands of HUF; However for trust it will not be treated as application of income as only expenditure incurred by registered trust on specified charitable objects as per object clause in trust deed will be allowed as application of income. The trust cash balance will be wiped-off from their accounts and XYZ HUF cash balance will increase.

Further in case two i.e. where Mr. X member of HUF is also trustee of said trust. In such case also the taxability of the above transaction will be same as case one.