- What is Section 194N

According to Finance Act, 2020 read with various notification issued from time to time new section i.e. 194N is applicable in case of cash withdrawals of more than Rs 1 croreduring a financial year. Further this limit will be reduced to Rs. 20 Lahks in case where ITR for immediately three consecutive previous years has not been filed within the time limit specified under section 139(1). This section will apply to all the sum of money or an aggregate of sums withdrawn from a particular payer in a financial year. The amendment in section is applicable from 1st July, 2020.

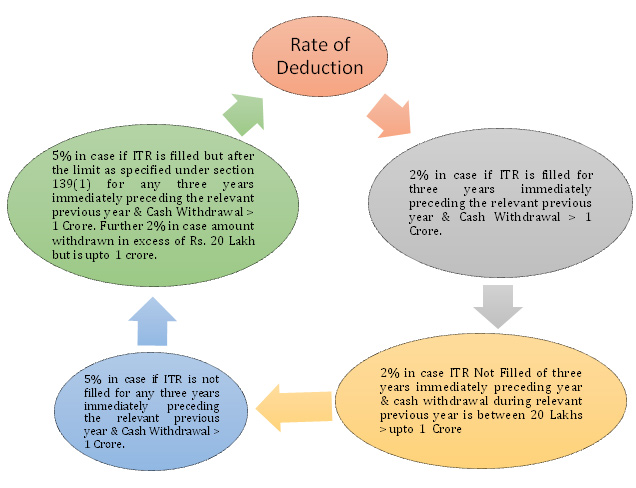

The rate for deduction will be 5% in case where withdrawal amount is exceeding Rs. 1 crore during the financial year and ITR for immediately three consecutive previous years has not been filed within the time limit specified under section 139(1). Further in that case if withdrawal is less than Rs. 1 crore but it is more than Rs. 20 lakhs then in that case TDS will be deducted at the rate of 2%. However, if assessee has filed ITR for three consecutive previous years within the time limit specified under section 139(1);then in that case TDS will be deducted only when withdrawal amount is exceeding Rs. 1 crore during the financial year and rate of deduction will be 2% in that case.

Illustration:

- Mr. R has filed return of income for three consecutive previous year however, in between one return was filed after the limit specified under section 139(1) i.e. belatedly. During the year Mr. R has withdrawn Rs. 36,00,000/- from bank Mr. R is of the opinion that as he has filled the return for three consecutive previous year TDS will be deducted only in case where withdrawal amount exceeds Rs. 1 crore. Determine whether contention of Mr. R is valid?

Answer : In the given case even if one return has been filed belatedly then in that case also the limit which will be applicable to assessee will be of Rs 20 lakhs and not of Rs. 1 crore. The rate of deduction will be 2% for amount withdrawn in excess of Rs. 20 lakhs but up to Rs. 1 crore; and 5% in case where amount withdrawn is in excess of Rs. 1 crore.

- Mr. J has filed return of income for three consecutive previous year within the limit specified under section 139(1). During the year Mr. J has withdrawn Rs. 1,24,00,000/- from bank. Bank has deducted TDS on entire withdrawal. Whether action taken by bank is valid in term of law?

Answer : In the given case action taken by bank is invalid as limit provided under section 194N in exemption limit that is TDS will be deducted only on excess amount. Therefore, in given case TDS will be deducted on Rs. 24,00,000/- and the rate applicable for deduction will be 2%.

- Mr. S has filed return of income for three consecutive previous year however, all the return filed by Mr. S are after the limit specified under section 139(1) i.e. belatedly. During the year Mr. S has withdrawn Rs. 13,00,000/- from X bank and Rs. 16,00,000/- from Y bank. Mr. S is of the opinion that as he has filled the return for three consecutive previous year TDS will be deducted only in case where withdrawal amount exceeds Rs. 1 crore. Also, he is of the opinion that limit will be applicable per bank and not on the basis of assessee. Determine whether contention of Mr. R is valid?

Answer : In the given case contention of Mr. S is partially valid as it has been specified by the department that limit specified under section 194N will be limit based on bank and not based on assessee.Further, if assessee has not furnished return of income for three consecutive years as per time limit specified under section 139(1) then in that case the TDS will be deducted on amount withdrawn in excess of Rs. 20,00,000/- but up to Rs. 1,00,00,000/- at the rate of 2% and at the rate of 5% in case of withdrawal in excess of Rs. 1,00,00,000/-.

- To whom it will be applicable

- Whether there is any exception to the above section?

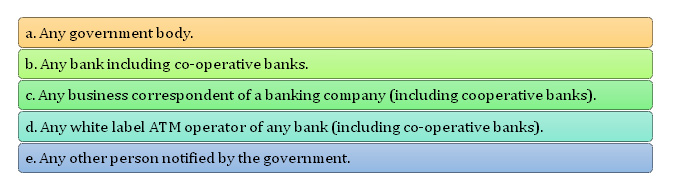

According to section 194N it will not be applicable to the withdrawals done by:

- Whether there is any amendment to section 194N?

i) If the assessee hasn’t filed the income tax return for any of the three consecutive previous year with the time limit specified under section 139(1) : In that case rate of deduction will be 2% on the amount withdrawn in excess of Rs. 20 lakhs up to Rs. 1 crore withdrawn while 5% applicable on the amount exceeding the INR 1 crore of the financial year.

ii) If the assessee has filed the income tax return for the given year : TDS deduction applicable only at the rate of 2% on amount withdrawn in excess of Rs. 1 crore.Therefore, if assessee wants to avail the benefit of reduced rate then Income Tax return for three consecutive year must be filed within the specified time period as per section 139(1). Further any enterprise which is newly registered will not get the benefit of such provision as in that case track record of filing of ITR will be nil and therefore they will not be eligible to get the benefit of the above condition.

Illustration : M/s G and Traders is a newly registered firm. From1st July,2020 to 20th July, 2020 it has withdrawn an amount of Rs. 1,00,000/- on daily basis; Mr. G proprietor of such entity is of the opinion that as they are newly registered entity, they will get have the cash withdrawal exemption of Rs. 1,00,00,000/- and not of 20,00,000/-. Determine whether contention of Mr. G is valid or not?

Answer : Contention of Mr. G is not valid as limit of Rs. 20,00,000/- will be applicable and not of Rs. 1,00,00,000/-. Because as per section 194N the reduced rate will be applicable only in the case where Income Tax return for three consecutive year has been filed within the specified time period as per section 139(1). In case of newly registered enterprise their track record of filing of ITR will be nil and therefore they will not be eligible for benefit of the above condition.

- Important points:

- TDS will be deducted by the payer while making the cash payment over and above Rs 1 crore in a financial year to the payee or 20 Lahks in case where ITR for three consecutive previous year has not been filed within the limit specified in section 139(1). Further, the TDS will be deducted on the amount exceeding Rs. 1 crore or 20 Lahks in case where ITR for three consecutive previous year has not been filed within the limit specified in section 139(1). Therefore, if a person withdraws Rs. 95,00,000/- in the aggregate in the financial year and in the next withdrawal in the same financial year, is of Rs. 5,50,000/- then in that case TDS liability is only on the excess amount of Rs. 50,000/-.

- The purpose of cash withdrawal, whether for business or personal, is irrelevant.

- Bank-wise threshold limit: The limit of Rs. 1 crore shall apply bank-wise and not branch-wise. This is possible now due to core banking solutions implemented by banks.

- Aggregate from all accounts: It shall apply if the aggregate amount of cash withdrawal in a financial year exceeds Rs. 1 crore from one or more bank accounts. In other words, the aggregate of cash withdrawal from the savings account, current account, cash credit account, overdraft account, etc. of the same person shall be aggregated to determine the threshold limit of Rs. 1 crore or Rs. 20 lakhs, as the case may be.

- TDS shall apply on excess cash withdrawal: If the cash withdrawal amount in a year exceeds Rs. 1 crore or Rs. 20 Lakh then TDS will apply on the excess amount of cash withdrawal over Rs. 1 crore or Rs. 20 Lakh, as the case may be, and not on the entire amount of cash withdrawal.

- Rate with respect to conditions: