- Introduction:In current choice of investment avenue can make or break the realisation of financial dreams. It is because of the forces of inflation and taxes. These tend to reduce the purchasing power of your money and impede faster wealth accumulation. Along with percentage of return one needs to understand what will be the taxability of gains derived by him from shares or mutual funds.

- Provision relating to Taxation of Dividend and Gain on Sale of Equity shares:

Dividend received by assessee in F.Y. 2020-21:The domestic companies shall not be liable to pay DDT on dividend distributed to shareholders on or after 01-04-2020. However, domestic companies shall be liable to deduct tax under Section 194. As per the Section 194, which shall be applicable to dividend distributed, declared or paid on or after 01-04-2020, an Indian company shall deduct tax at the rate of 10% from dividend distributed to the resident shareholders if the aggregate amount of dividend distributed or paid during the financial year to a shareholder exceeds Rs. 5,000. However, no tax shall be required to be deducted from the dividend paid or payable to Life Insurance Corporation of India (LIC), General Insurance Corporation of India (GIC) or any other insurer in respect of any shares owned by it or in which they are beneficial owners. However, where the dividend is payable to a non-resident or a foreign company, the tax shall be deducted under Section 195 in accordance with relevant DTAA (Double Taxation Avoidance Agreement). Therefore, now dividend will be taxable and regular income under the head ‘Income from other sources. Further deduction is allowed for interest expense incurred against the dividend. The deduction should not exceed 20% of the dividend income received. However, you cannot claim a deduction for any other expenditure incurred for earning the dividend income.

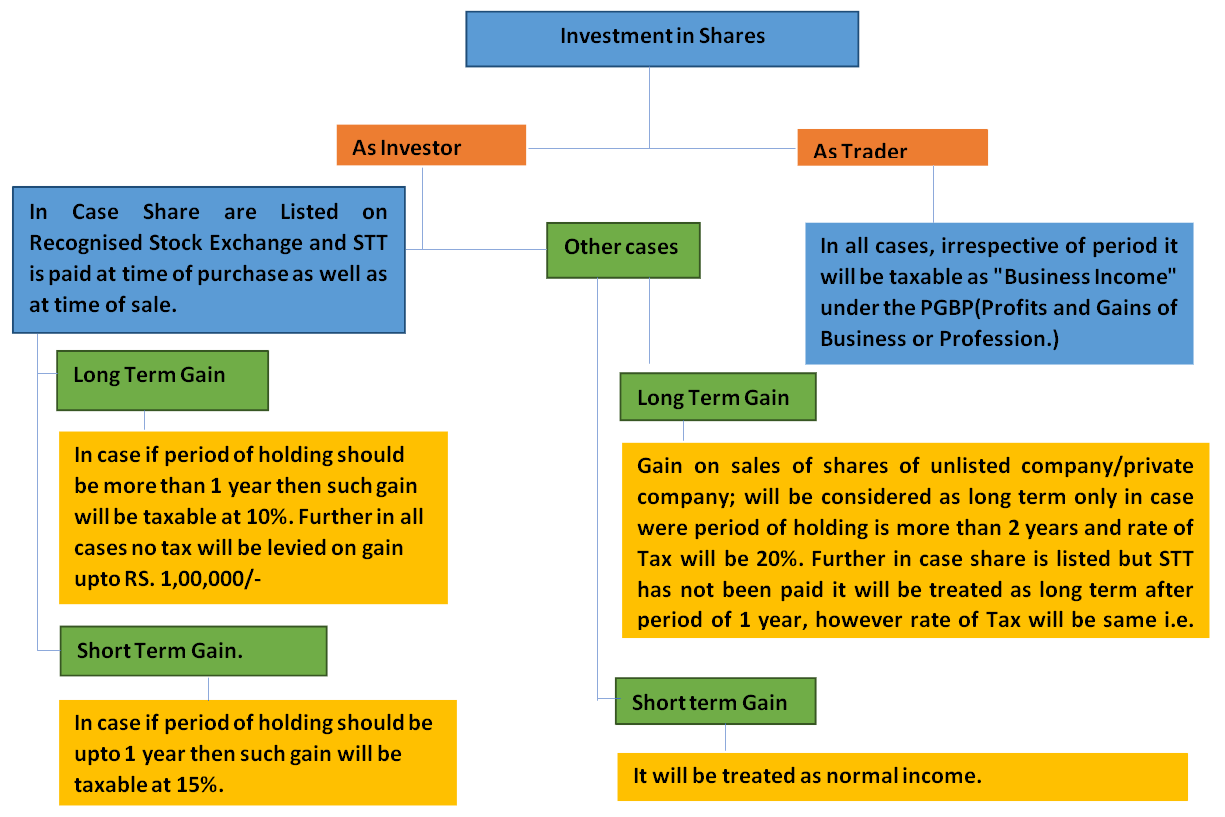

Taxability of gain on sale of equity shares for F.Y. 2020-21:

In case there is long-term capital gains from sale of listed securities to a non-resident investor acquired through foreign currency then in that case computation of gain will be in different manner and such gain will be taxable at the rate of 10% without allowing any indexation.

-

- Provision relating to taxability of income distributed by mutual fund and capital appreciation on units :

Equity oriented fund :

Sale of units :

In case of equity-oriented fund it will be qualified as long term if it is held for more than 12 months and such gain will be taxable at the rate of 10% in hands of individual on amount in excess of Rs. 1,00,000/- amount. Further if it is short term gain then it will be taxed at the rate of 15%.

Debt oriented fund :

Sale of units :

Debt mutual funds have to be held for more than 36 months to qualify as a long-term capital asset. If redeemed within three years, the capital gains will be added to your income and will be taxed as per your income tax slab rate. Long term gain will be taxable at the rate of 20% with indexation.Income distributed by above mutual fund in form of dividend will now be taxed in hands on recipient i.e. after removal of concept of DDT any interim income distributed by mutual fund will be taxed in hands of investors

- Important issues:

Sweat equity shares : Sweat equity shares are shares orspecified securities issued at discount or for consideration other than cash to employees or directors of the company as reward their hard work or for their value addition in the progress of the company.This share provided will be taxable as perquisite in the hands of employees in previous year in which shares or securities are allotted or transferred to the employee.

Valuation of such will be as follows:

Quoted Shares:

If the shares of the company are listed on any Stock Exchange :

Fair market value (Average of opening and closing price on date of exercise) In case there is shares are listed on more than one exchange then average value will be taken from exchange which has highest volume of trading of shares of the company.

In case there is no trading of shares on date of exercise of option,then the Fair Market Value will be the closing price of the shares on any stock exchange on date immediately preceding day to date of exercise on option on which trading was undertaken.

Unquoted Shares:

If the shares of company are not listed on any stock exchange then the fair market value of shares will be as determined by the Merchant Bankers on the Specified Date.

“Specified Date”; means the date of exercise of the option, or any date earlier the date of exercise of the option, not being a date, which is more than 180 days earlier than the date of excursive of the option.When such share is sold by the employee gain will be taxed at rate mentioned in point 2.

Bonus Shares : Bonus shares are new shares issued to existing shareholders of a company. These shares are issued to the shareholders in proportion of their current holdings.

Bonus share received will be taxable as rate provided in above point no. 2, at time of sale and no tax will be levied at time of allotment of such shares. Also, it is important to note that cost of acquisition of bonus shares is taken as zero hence the capital gain on selling a bonus share is equal to its selling price. Further while calculating period of holding it would be calculated separately for original shares and bonus share. For Bonus share period of holding will begin from date of allotment of shares

Right Shares : Right shares provides right to existing shareholders to acquire more shares in the company at a price which is lower than the current market price.

Taxability of right share will be divided into two parts:

Where right is renounced: In this case the amount received from renouncing right shares will be fully taxable and cost of acquisition for this purpose will be taken as Nil.The period of holding will be considered from the date of offer to subscribe to shares to the date when such right entitlement is renounced by the person. Generally, this type of gain is short term and therefore it is clubbed with other normal income and is taxed at normal slab rate.

Where right is exercised: In case right is exercised then it will be taxable at rate mentioned in point no. 2 and period of holding will begin from date of allotment, further cost for this purpose will be exercise price paid. In case any person has purchase right renounced by other person then in that case cost will be consideration paid for purchase od renounced right along with exercise price paid.

Split of Shares:

Stock split is a corporate action to increase the number of outstanding shares by issuing more shares to existing shareholders.There is no increase in the market capitalization of the company, hence post-split, price of the stock decreases in reverse ratio of split.

Taxation in case of Split of share: The provision for taxation of split is slightly different from bonus, here cost of acquisition will be determined by dividing original cost with total no. of share (i.e. after spilt). Further period of holding will be calculated from date of acquisition original share. Then such gain will be taxable as per rate mentioned in point no. 2.

Buyback of Share :

Many companies in view that their share is undervalued; they carryout procedure of buyback.

Taxation of Buyback of share :

For shares of unlisted company: As per section 115QA of the Income Tax Act; company will be required to pay a levy of additional Income-tax at the rate of 25% of the distributed income on account of buy-back of unlisted shares by the company. As additional income-tax has been levied at the level of the company, the consequential income arising in the hands of shareholders has been exempted from tax under section 10(34A) of the Income Tax Act.

For shares of Listed company: There will be simple calculation taking amount received on account of buyback as consideration and deducting acquisition cost from it; Further, period of holding shall be from the date of acquisition to the date of Buy-Back. Rate of tax will be determined in accordance with point no.

- Classification of asset based on period of holding:

| Asset | Period of holding | Short Term / Long Term |

| Immovable property | Up to 24 months | Short Term |

| >24 months | Long Term | |

| Listed equity shares | Up to 12 months | Short Term |

| >12 Months | Long Term | |

| Unlisted shares | Up to 24 months | Short Term |

| >24 months | Long Term | |

| Equity Mutual funds | Up to 12 months | Short Term |

| >12 months | Long Term | |

| Debt mutual funds | Up to 36 months | Short Term |

| >36 months | Long Term | |

| Other assets | Up to 36 months | Short Term |

| >36 months | Long Term |